🪙 This Script keeps you POOR

+ How to change it

Let me tell you the story of an ordinary life.

You’re born.

Your parents immediately start saving for your education.

You go to school.

Then tutoring classes.

Then university.

You take a student loan. Because of that degree, you get a job.

First month of salary: “Oh, you got a job? You need a car now.”

So you take a car loan.

Then someone says credit cards are great.

You get rewards.

You build a credit score. So you get one.

Then comes the relationship.

The proposal.

The wedding.

Expenses pile up.

You take a personal loan to cover it all.

You feed hundreds of guests for two days like there’s no tomorrow.

Then comes the house.

Because renting is “throwing money away.” So you take a mortgage.

By age 28, you have 20-25 years of debt sitting on your head.

30-40% of your salary goes into monthly payments.

Mortgage.

Car loan.

Personal loan.

Student loan still being paid off.

Then people ask: “When are you having kids?”

Kids arrive.

And you do exactly what your parents did, start saving for their education.

Except now, one month of daycare costs what your entire college semester used to cost.

Someone pushes an insurance policy on you.

Someone else pushes an investment product.

A financial app is already running on your phone.

Life is completely packed with payment after payment.

And here’s the most insane part:

Almost everyone, everywhere in the world, is living this exact same life.

Who Wrote This Script?

Think about it.

Someone, somewhere, sat down and thought:

“Let’s get them into university. Then make them buy a car. Then get them married with a loan. Then a mortgage. Then kids. Then more debt.”

This script was not written for your happiness.

It was not written for your security.

It was not written so you could become wealthy.

It was written so someone else could profit from your life.

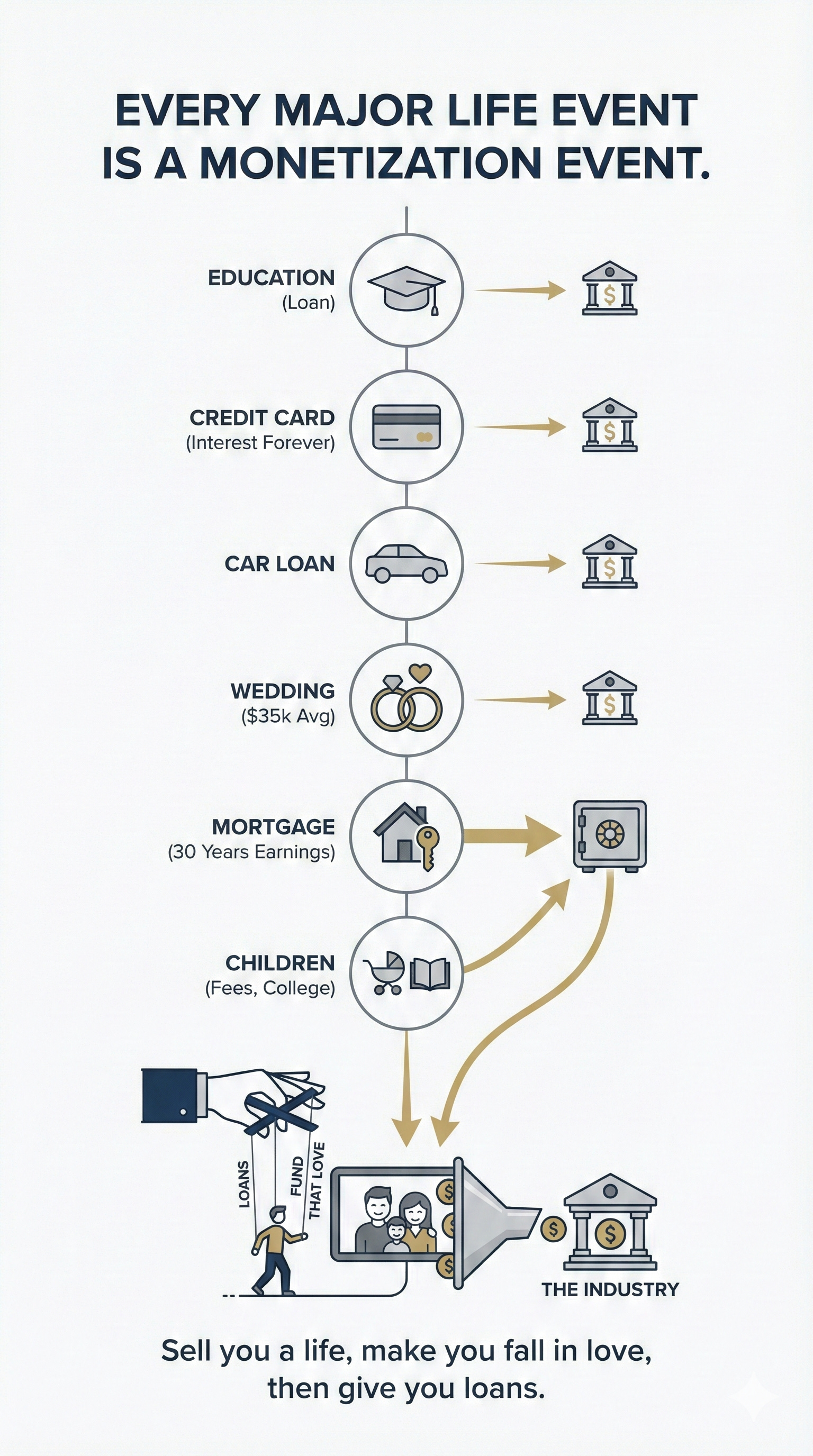

Every major life event you have?

It’s a monetization event.

Your education: monetization event

Your first credit card: monetization event (pay the minimum, keep paying interest forever)

Your car loan: monetization event

Your wedding: monetization event (average US wedding now costs $35,000)

Your mortgage: 30 years of earnings handed over to a bank

Your children: school fees, tutoring, daycare, college savings, another monetization event

An entire industry exists whose only job is to sell you a life, make you fall in love with that life, and then give you loans to fund that love.

The Marketing Machine Behind It All

This doesn’t happen by accident.

Banks and financial institutions spend hundreds of billions of dollars every year on advertising globally.

Just to tell you:

“We have loans. Your Dream House is within reach. Your Dream Car is waiting. You deserve it.”

They know your age.

Your income.

Your browsing habits.

Your desires.

They know what will make you click.

What will make you feel like you’re missing out.

What will make you say yes.

And this story is old.

Credit cards used to be for the wealthy elite only.

Having an American Express card in 1980 meant you had truly arrived.

Today?

An 18-year-old gets credit card offers in the mail before they’ve earned their first paycheck.

Mortgages used to require 20-30% down payments.

The message was: “Save first. Then buy.”

People bought homes in their 40s.

Then banks got creative.

Down payments dropped.

Interest rates fell.

New loan products appeared.

The message changed overnight:

“Own your dream home NOW.”

The median age of first-time homebuyers in the US is now 38.

In the UK, it’s 34.

Both are record highs.

But the average age of buying a first home a generation ago?

Early to mid 30s, with far less debt attached.

The loans got easier.

The trap got bigger.

“You Deserve It” — The Three Most Dangerous Words in Finance

At some point, the financial industry discovered something powerful:

Guilt-free permission to spend.

“You work hard. You deserve it.”

“Life is short. Treat yourself.”

“Why wait? You can have it now.”

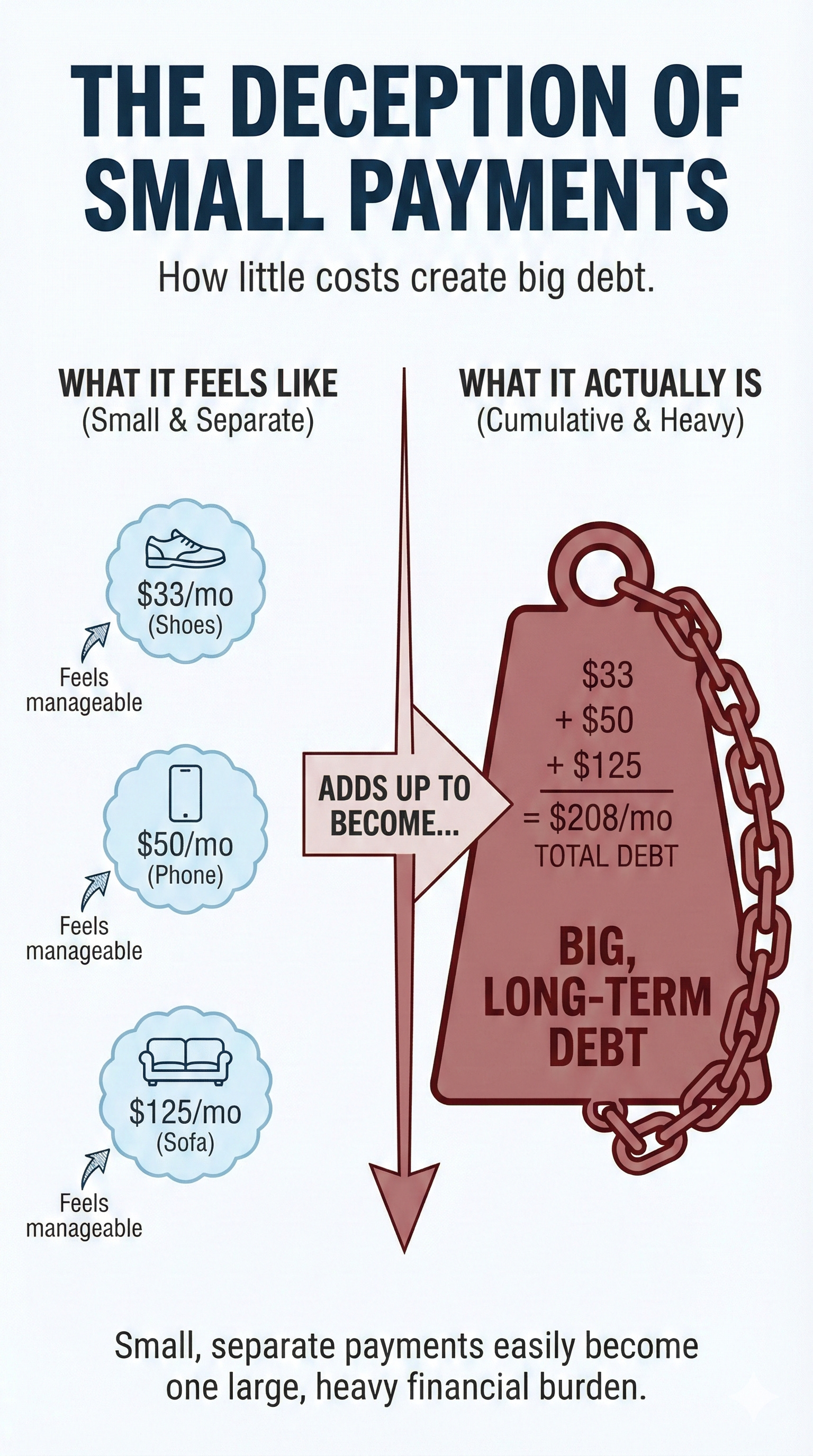

Buy Now Pay Later (BNPL) exploded globally.

Companies like Klarna, Afterpay, and Affirm made it possible to split any purchase into easy installments.

That $400 pair of shoes? Just $33 a month.

That $1,200 phone? Just $50 a month.

That $3,000 sofa? Just $125 a month.

Sales exploded everywhere.

And what did this do to us?

The things we used to save up for and buy carefully?

We now buy impulsively because the payment feels small.

$33 a month doesn’t feel like $400.

But it is.

And it adds up across every purchase you make.

“Settle Down” Is a Business Model

Everywhere in the world, society has one message once you hit your mid-20s:

“Settle down.”

Finish studies → Settle down.

Get a job → Settle down.

Buy a car → Settle down.

Get married → Settle down.

Buy a house → Settle down.

Have kids → Settle down.

“Settling down” is a business model.

Every single event has a financial outflow attached to it.

When society tells you to “settle down,” what they’re really saying is:

“Are you ready to transfer your hard-earned money to banks, loan companies, and vendors?”

Think about it:

Average US wedding: $35,000

Average UK wedding: £20,000

Average Australian wedding: $36,000

Many couples go into debt specifically for one day

Where does this money come from?

Parents’ retirement funds. Personal loans. Years of savings.

All transferred to the financial industry in one weekend.

The Numbers Don’t Lie

US household debt hit a record $17.5 trillion in 2024.

The average American carries:

$6,000+ in credit card debt

$19,000+ in car loans

$38,000+ in student loans

$240,000+ in mortgage debt

And it’s not just America.

UK household debt is over £2 trillion.

Australia’s household debt-to-income ratio is one of the highest in the world.

In emerging markets across Asia, Africa, and Latin America, consumer lending is growing at record rates.

The script is global.

And salaries?

Growing at 3-5% annually in most developed countries.

Real inflation in our actual lives (eating out, education, technology, healthcare, housing)? Much higher.

The official inflation numbers don’t capture what most people actually spend money on.

So in real terms, purchasing power is shrinking.

And the response everywhere is the same: More debt.

The Goalpost That Never Stops Moving

Here’s what nobody tells you:

When you earn $30,000, you think everything will be fine at $60,000.

At $60,000, you think you need $100,000.

At $100,000, you think you need $150,000.

Satisfaction never comes.

Why?

Because every time your income goes up, the script tells you to upgrade your lifestyle.

Bigger house.

Better car.

More expensive holidays.

Designer clothes.

This is called lifestyle inflation.

And it’s one of the most powerful traps in the world.

And when lifestyle inflation outpaces income growth, three dangerous things start to happen:

1. Get-Rich-Quick Schemes Look Attractive

Crypto.

Options trading.

Day trading apps.

Overnight investment schemes.

Educated, smart people fall for obvious scams.

Why?

Because at some point they genuinely believe that unless money is made fast, they’ll never win the race they’re running.

It’s not stupidity.

It’s desperation born from a broken system.

2. “Safe” Things Look Attractive (But They’re Also Failing You)

Savings accounts earning 1-2% while inflation runs at 6-7%.

Money sitting in low-interest accounts quietly losing purchasing power every year.

Your money is rusting.

Insurance products that earn terrible returns while agents pocket massive commissions.

Years later you realize nothing is working.

The agent has long moved on.

You got nothing.

3. Buying a House Too Early

Property is considered the best investment everywhere.

But here’s the truth:

Most people didn’t become rich because of real estate. They became rich and then invested in real estate.

That’s the actual sequence.

For someone who takes a 25-30 year mortgage at 27, locking themselves in when their salary is smallest, their flexibility is greatest, and their life is most uncertain,

It often doesn’t make financial sense.

Buying a home can be a wonderful decision.

It may be the best financial move of your life.

But at the right time.

Buy too early and you’re chaining yourself for the wrong reasons.

You don’t know where you’ll want to live in 10 years.

You don’t know how your life will change.

Buy when you actually know what your life looks like.

Who Is Winning From Your Life?

Let’s name them:

Banks — take your deposits and lend them back to you as mortgages, car loans, personal loans, student loans

Credit card companies — give you a loan at 20-30% interest when you pay the minimum

Buy Now Pay Later companies — make impulse purchases feel painless

Education institutions — convince you that without the right degree from the right school, your life is ruined

Tech companies — release a “best ever” phone model every 12 months

Car companies — make you feel unsuccessful without the latest model

Wedding industry — make you spend $35,000 on one day

Social media — shows you a highlight reel of everyone else’s spending to make you feel behind

All of them profit from your life.

Using your money.

The Question You Need to Ask Yourself

Here’s a powerful exercise:

Imagine nobody is watching you.

No society.

No parents.

No friends.

No Instagram.

No LinkedIn.

How would you live?

Would you still buy that car with a loan?

Would you still have a $35,000 wedding?

Would you still lock yourself into a 30-year mortgage at 27?

Would you still upgrade your phone every year?

Or would you live differently?

The Math of Financial Freedom

Here’s something simple but powerful.

In most countries, if you have a portfolio of $500,000 - $1,000,000 invested in diversified index funds earning 7-8% annually:

That’s $35,000 - $80,000 per year in passive returns.

Without touching the principal. Ever.

For many people in lower cost-of-living areas, or with modest lifestyles, that’s enough to live comfortably.

The question is: What do you need to do to get there?

And how fast can you get there?

With today’s salaries and investment tools, it’s more achievable than you think.

If you consciously refuse to follow the script.

If you don’t turn every life event into a monetization event for someone else.

If you stop mistaking advertisements for life advice.

Rewrite Your Script

Here’s what I want you to take away:

Your life is very profitable.

The only question is: Is it profitable for you, or for someone else?

You don’t have to live like a monk. You don’t have to deprive yourself of everything.

But look at the script you were handed at birth.

Which parts of it actually suit you?

Which parts did you choose, and which parts were chosen for you?

The wedding you wanted, or the wedding society expected?

The house you needed, or the house that would impress the neighbors?

The car you required, or the car that would signal success?

The degree you chose, or the degree that sounded impressive?

Ask these questions before you sign the next loan.

Because every monthly payment you take on is time you’re selling to someone else.

And time is the one thing you can never get back.

Your Assignment This Week

Answer these three questions honestly:

1. List every loan or monthly payment you currently have.

How much of your monthly income goes toward debt payments?

Is it over 30%? Over 40%?

2. Which of these were truly your choice?

Which were social pressure?

Which were because “everyone does it”?

Which were because an ad made you feel inadequate without it?

3. What would your finances look like if you had said no to just one of them?

Calculate it.

The number might surprise you.

Hit reply and tell me: What’s the one part of the script you wish you had questioned earlier?

I read every response.

And I promise you’re not alone in this.

Talk soon,

Your Bank account will thank you later.

Resources to help you get started:

Money Rules Cheat Sheet - Quick reference guide for the fundamentals

Wealth Building Resources - My curated collection of books, courses, and tools

Premium Newsletter Access - What the top 1% are reading

~ Be Wealth Operator

P.S. Your life is not a monetization event for someone else’s profit. It’s time to start treating it that way.

P.S.S. Quick note: I'm not a financial advisor, and this isn't financial advice. I'm sharing my personal experiences and research for educational purposes only. Please consult a qualified financial professional before making investment decisions, and always do your own research.

I hope more people resist these lifestyle /financial traps

and resist being slaves to debt

Very powerful. I will write a post in Dutch about this “debt trap”, and how to escape it.